Learn how insurance archeology can locate an organization’s old insurance to help pay for legal fees and settlements

By David A. O’Neill, J.D.

Last year, Governor Andrew Cuomo signed the Child Victims Act in New York. One of the provisions of the Act provided victims the ability to file previously time-barred cases for a period of one year. However, due to COVID-19, and the pandemic’s impact on court processes, the Senate and Assembly have extended the victims’ deadline to file claims to August 14, 2021.

Across the nation, sexual abuse claims present both moral and financial challenges to organizations involved in litigation regarding possible misconduct in decades past. The allegations most prominently involve improper behavior by teachers, former staff, priests, and ministers in the 1950’s, ‘60’s and ‘70’s. The alleged victims’ recollections have long laid dormant and often come as a shock to modern day school and church administrators.

In my experience as an insurance archeologist, I have successfully assisted many churches and schools whose present pastors and head masters have found themselves targeted in litigation based on a former church goer’s or a former student’s recollections of sexual abuse. I have also worked to locate historical policies issued to organizations and institutions with a focus on children’s welfare issues.

As an insurance archeologist, we are typically called in after attorneys, insurance brokers, and school officials have been consulted. The attorney has directed his or her client to pull together any historical documents it may have relating to insurance during the years that, according to the complaint, the misconduct occurred. The current insurance broker has been notified of a potential claim and has been asked to identify possible coverage.

If the client is unable to find proof of insurance, the insurance broker advises that current insurance does not cover long-tail claims and it cannot identify the earlier insurance policies, then an insurance archeologist is called in to locate the historical insurance policies.

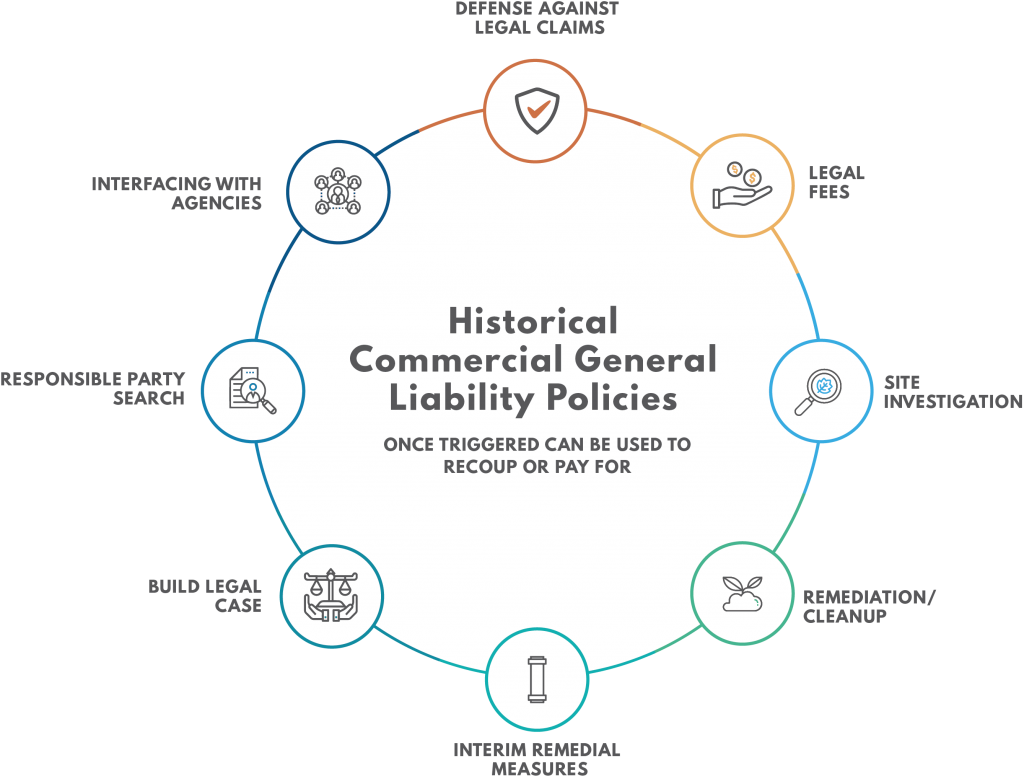

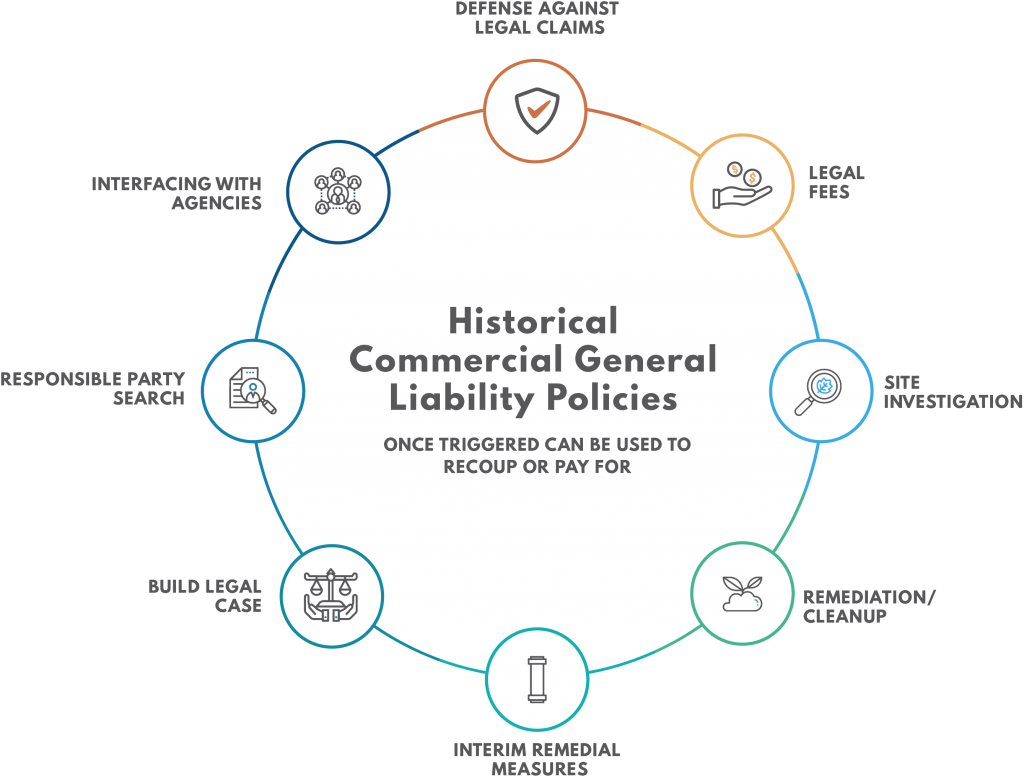

Sexual misconduct coverage can be found in the general liability policies covering either the entire institution or the particular school or church in which the occurrences took place. Unlike environmental and asbestos exposures that are often ongoing, sexual abuse exposures can be intermittent. Occurrences on separate dates in the same month can trigger coverages under separate policies.

The work of an insurance archeologist is always confidential. Often the investigation is performed at the direction of attorneys defending the church or school, and the report of findings is an attorney work product, considered protected as an attorney-client privileged document.

Usually on my initial meeting with church or school administrators, I find them still in shock about the entire matter. They are young people doing good work with children, the mentally challenged, the elderly and those in need. They are consumed by a legitimate worry for the survival of their particular institution or organization. They often don’t understand why the insurance broker’s records do not go further back in time and have searched their records and could not find their old policies.

There are two main parts to insurance archeology. First, we conduct archival searches and interviews to find leads concerning historic policies, and then we follow up on those leads to identify carriers that issued general liability policies that can provide funding to respond to abuse claims.

While no individual document provides the whole story, a good insurance archeologist knows how to assemble their findings to approximate a skeleton of the historical insurance program. Lastly, in a meeting with the attorney, the insurance archeologist identifies which insurance carrier(s) to place on notice and provides the insurance evidence to attach to the notice of claim.

Insurance archeology can help the school or church administrators find funding for legal fees and settlements to address sexual abuse claims. With the extension of the Child Victims Act until 2021, it’s highly probable that administrators will still receive claims. By taking a proactive approach and working with an insurance archeologist, missing or lost pieces of historical coverage information can be located to provide a full picture of your organization’s historical insurance coverage.

Contact us today to learn about confidential insurance archeology.

David A. O’Neill, Director of Investigations

David O’Neill has over 20 years of experience in claims recovery on behalf of corporate policyholders involving environmental property damage and toxic tort and asbestos exposure claims. He is an accomplished insurance archeologist with extensive experience in locating and retrieving insurance coverage evidence on behalf of potentially responsible parties responding to environmental investigation and remediation demands.

Mr. O’Neill is also an experienced PRP investigator with knowledge of CERCLA/SARA requirements, having conducted over thirty PRP searches at Superfund hazardous waste sites for PRP defense counsel and previously for USEPA Regions V and VIII. Mr. O’Neill was formerly Insurance Research Manager for Risk International Services, Inc. He graduated from Case Western Reserve Law School in 1986.